The Cook County Department of Revenue's Tactics Should Be Investigated

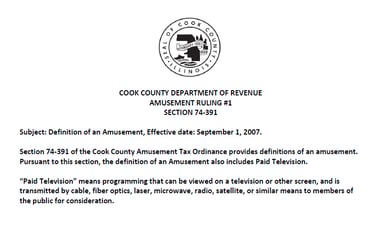

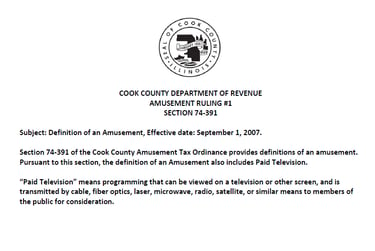

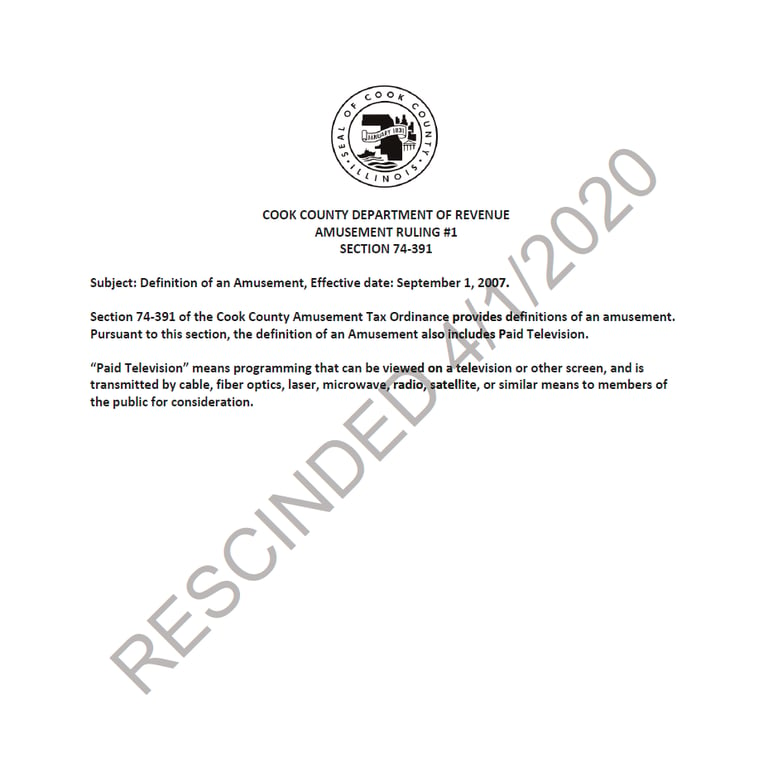

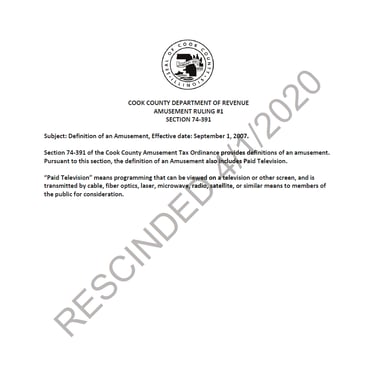

In 2007, Cook County Department of Revenue's management issued Amusement Ruling #1 that stated Section 74-391 of the Cook County Amusement Tax Ordinance provides definitions of an amusement and that pursuant to that section, the definition of an amusement also includes Paid Television. The effective date on it was September 1, 2007. CCDOR presented Ruling #1 to businesses, and notified them that they owed Cook County Amusement Taxes on Paid Television.

CCDOR's Ruling #1 :

There are a couple of major issues regarding CCDOR's Ruling #1. The Ruling's declaration that the Ordinance's definition of an amusement, Section 74-391, includes Paid Television is a false statement. The Amusement Tax Ordinance which was enacted in 1996, and has been in effect since February 1, 1997 has never included "Paid Television" or anything similar to it in its definition of amusements.

If CCDOR contends that Ruling #1 was their way of adding Paid Television to the definition of an amusement, then CCDOR was exceeding its authority. CCDOR's management does not have the authority to add language to the Amusement Tax Ordinance only the Cook County Board of Commissioners has that authority.

CCDOR's management knew they did not have this authority as is evidenced by the 2 failed attempts they made proposing amendments to the Board of Commissioners to include Paid Television as a form of an amusement in February of 2011, and then again in November of 2015.

February 2011 was the first time CCDOR's Director proposed an amendment to include Paid Television in the definition of an amusement in Cook County's Amusement Tax Ordinance. One of the reasons the Director gave for the amendment was "...in the interest and fair and equitable enforcement [CCDOR] seeks to clarify significant definitions..."

In the February 2011 board hearings, the Cook County Board of Commissioners declined to add "Paid Television" in the definition of an Amusement and also declined to add a section defining "Paid Television". After the Board's decision, CCDOR did not stop, but continued to use Ruling #1 to aggressively pursue businesses for amusement taxes on Paid Television, and CCDOR continued to collect this tax from businesses that it had already convinced into paying.

In November 2015, the Director of CCDOR attempted yet again to add Paid Television into the definition of amusement in the Amusement Tax Ordinance. This time the reasons were the following:

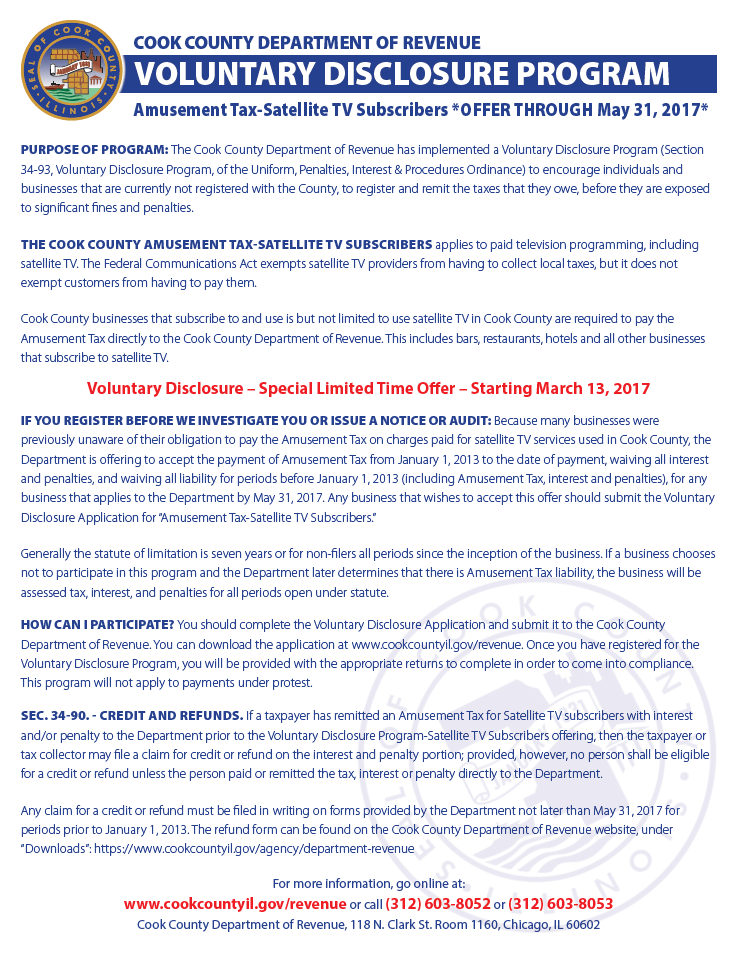

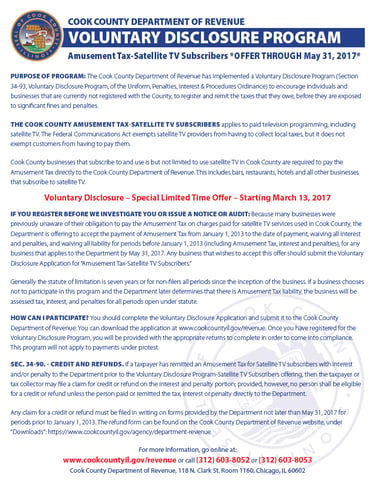

CCDOR "encourages individuals and businesses ...to remit the taxes that they owe, before they are exposed to significant fines and penalties."

It also states that it applies to paid television programming and "the Federal Communication Act exempts providers from having to collect local taxes, but does not exempt customers from having to pay them."

The letter claims that businesses that use satellite TV "are required to pay the Amusement Tax directly to the CCDOR."

CCDOR uses bold red text to emphasize this "Special Limited Time Offer"

CCDOR informs businesses that "If you register before we investigate you or issue a notice of audit", because "...Many businesses were previously unaware of their obligation to pay the Amusement Tax.." CCDOR was also informing businesses to remit four years worth of back taxes by calculating their payments starting from January 1, 2013.

CCDOR continues to inform businesses that "If a business chooses not to participate in this program and the Department later determines that there is Amusement Tax liability, the business will be assessed tax, interest, and penalties for all periods open under statute."

CCDOR created voluntary disclosure file numbers for the nearly 700 businesses they assumed had Paid Television and also force registered all of them for amusement tax without the businesses' consent. This forced registration meant that all of these businesses were now registered as being Amusement Tax Operators in CCDOR 's RPE (Revenue Premier Enterprise) database and now had a duty to file tax returns and to remit Amusement Taxes, and if they did not they would receive delinquency notices.

So hundreds of businesses ended up signing up for this "Voluntary Disclosure Program", and began paying amusement tax on Paid Television/Satellite TV.

For business that disregarded CCDOR's "Voluntary Disclosure Program" letter and never made any amusement tax payments, CCDOR ended up closing their accounts from their RPE database. Therefore, businesses that ignored CCDOR paid absolutely nothing, but businesses who believed in CCDOR's Ruling #1 and the voluntary disclosure program's false statements collectively paid over 3 million dollars of amusement taxes to CCDOR. That is neither fair nor equitable.

During this period, CCDOR was a party to another administrative hearing case involving Paid Television. It was on December 1, 2016, that an auditor from CCDOR, relying on Ruling #1, issued a Notice of Jeopardy Tax Determination and Assessment of amusement tax due on Paid Television to Palmer House Hotel. Attorneys for Palmer House filed a Protest and Petition for Hearing and a hearing with the Cook County Department of Administrative Hearings commenced. (Source: ALJ decision of Cook County v. Palmer House)

Midway through this case, CCDOR abandoned Ruling #1 as the basis of the assessment, probably because they had been told by the ALJ of the Comcast case that Ruling #1 was invalid and they knew they would lose again using that same argument. Instead, CCDOR now argued that the Amusement Tax Ordinance's definition of taxable amusement is broad enough to include "paid television" and as such, the Palmer House "is obligated to collect the tax from its guest[s] for the use of the amusement." (Source: ALJ decision of Cook County v. Palmer House)

CCDOR was well aware that the definition of a taxable amusement did not include Paid Television as is evidenced by the February 2011 and November 2015 Board Minutes, and with what the ALJ was telling them in the Comcast case.

This strategy where CCDOR makes up another argument, no matter how far-fetched, is very common with CCDOR. They have been utilizing this strategy in other amusement tax cases, and in cases involving other tax types. It is my belief that CCDOR's goal is not to try and win these cases with these arguments, but to prolong these cases as much as possible. I will explain why I believe CCDOR does this, and how I came to this conclusion below.

So lets get back to CCDOR's argument that the Palmer House Hotel and all of these other businesses they targeted were amusement tax operators and had an obligation to collect and remit this tax. CCDOR expected these businesses to collect these Amusement Taxes from people that were patrons of those businesses; People going out for a drink at a bar or to eat at a restaurant, people staying at a hotel, students attending universities, patients at hospitals, nursing home residents, …etc. They expected these businesses to take their Paid Television (Cable and/or Satellite TV) bills , calculate the amusement taxes on those bills, keep an eye on and track every single one of their patrons, and allocate a percentage of the tax to the customers that may have glanced at a television screen located in those businesses. And this tax would somehow "alleviate tax reporting burdens on area businesses" as was the explanation behind the Director's 2015 Amusement Tax Ordinance proposal.

On May 6, 2019, the Palmer House was granted a motion for summary judgment. The Administrative Law Judge, again concluded that Ruling #1 could not sustain the Assessment and explained that even if Paid Television fell within the Amusement Tax Ordinance's definition of a taxable amusement, Palmer House would still not have a collect-and-remit obligation, because it did not own, operate, or manage the amusement or the place where the amusement was being held. The ALJ also determined, yet again, that by issuing "Ruling #1" and presenting it to businesses, CCDOR was attempting to take over the legislative function of the Commissioners who are the only ones that have the authority to expand the definition of a taxable amusement to include Paid Television. (Source: ALJ decision of Cook County v. Palmer House)

After this May 6, 2019 decision, did CCDOR immediately notify businesses to stop paying the Amusement Tax on Paid Television? No, they did not.

CCDOR finally notified businesses to stop collecting Amusement taxes from patrons as of April 1, 2020, and the evidence of this is on their Amusement Tax website presented here:

CCDOR is admitting to the Board that this is an "already established practice" and uses terms such as "in order to alleviate confusion" and "will alleviate tax reporting burdens on area businesses" to justify their proposal, but in actuality this amendment would subject hundreds of businesses to an additional tax and the associated tax reporting burdens that go along with it.

During this November 2015 Board Hearing, The Board of Commissioners of Cook County again declined to add "Paid Television" to the definition of a taxable amusement, and they again voted to not include "Paid Television" in the definition section of the Amusement Tax Ordinance as the CCDOR Director was proposing.

Even after CCDOR's second failed attempt to get Ruling #1 into legislation, CCDOR continued to collect amusement taxes on Paid Television from businesses already registered, and they continued to contact other businesses and present to them Ruling #1 as proof that they are subject to Amusement Tax for Paid Television.

Around this time, CCDOR was also a party to an administrative hearing case involving Comcast and the Amusement Tax on "Paid Television".

In November of 2014, one of CCDOR's auditors notified Comcast that per Ruling #1 they should be registered as an Amusement Tax operator, and should be collecting and remitting the Amusement Tax on Paid Television. Comcast was told they would be given the opportunity to self-assess and pay this amusement tax liability beginning with the 2007 tax year. Comcast did not think they were subject to the Amusement Tax per the Amusement Tax Ordinance and declined to self-assess, so in May of 2015, CCDOR issued a Notice of Tax Determination and Assessment to Comcast seeking uncollected amusement taxes along with interest and penalties. Comcast protested this liability assessment and an administrative hearing case ensued. (Source: ALJ decision of Cook County v. Comcast)

The Administrative Law Judges in that case, relying on well-settled Illinois tax law, determined that CCDOR's Ruling #1 "was invalid because it extended by its plain language the scope of the Amusement Tax Ordinance's definition of a taxable amusement". (Source: Page 13, 14, & 15 of ALJ decision of Cook County v. Comcast)

After two unsuccessful attempts to get Paid Television into legislation and after an administrative law judge explained why Ruling #1 was invalid, one would think that CCDOR would finally get the point and they would stop pursuing businesses for Paid Television. Surprisingly, it had the opposite effect.

In early 2017, shortly after the ALJ's ruling on the parties' summary judgement motions (where the ALJ determined CCDOR"s Ruling #1 to be invalid), CCDOR's management came up with yet another idea of getting businesses on the hook for Amusement Tax on Paid Television. This time CCDOR would target "Satellite TV Subscribers". CCDOR rolled out a Voluntary Disclosure Program for Satellite TV Subscribers and sent out the following letter that is full of false statements and threats of significant fines and penalties to nearly 700 businesses. These businesses included bars, restaurants, hotels, universities, hospitals, nursing homes, and other businesses.

The Director also proposed adding a paragraph defining the term "paid television". This was the same exact way it was defined in CCDOR's Ruling #1.

The information on CCDOR's Amusement Tax website regarding paid television and boat rides/tours has not been altered since they posted it in April 2020. Unless CCDOR changes their webpage which is likely after the release of this report, you will still be able to find it at the following web address: www.cookcountyil.gov/service/amusement-tax

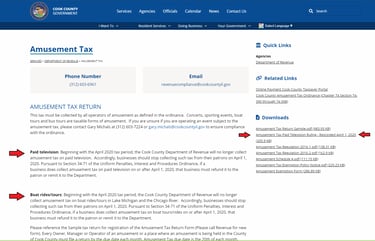

The webpage states that CCDOR will no longer collect amusement tax on paid television beginning with the April 2020 tax period and tells businesses to stop collecting from their patrons on April 1, 2020. It also states the same thing for boat rides/tours that were collecting amusement tax on boat rides/tours in Lake Michigan and the Chicago River.

The red arrows pointing to the "Amusement Tax Paid Television Ruling - Rescinded April 1, 2020" on the right is a pdf document which contains the following:

Between 2014 through 2020, CCDOR used similar unethical tactics for getting businesses to pay amusement tax on Boat Rides/Tours.

Since the 1996 enactment of the Cook County Amusement Tax and all the way to 2014, the amusement tax was never assessed to any businesses providing Boat Rides/Tours. In an October 6, 2000 letter from the Director of Revenue to an unspecified recipient, DOR stated, "it has been and still is the County’s position that both sightseeing cruises and water taxi services are not amusements as defined in the Ordinance and, therefore, are not subject to the tax.” In the summer of 2014, CCDOR changed its position and initiated an amusement tax compliance program, instructing its auditors to inform tour-boat operators that they needed to register with CCDOR as Amusement Tax operators and to begin collecting and remitting amusement tax payments. (Source: Appellate Court Opinion of Mercury Sightseeing Boats, Inc. v. County of Cook)

In August 2014, a CCDOR auditor contacted Mercury Sightseeing Boats, Inc. and Mercury Yacht Charters, Inc. (Mercury) and demanded that it register as an amusement tax operator, to collect and remit amusement tax, and to pay amusement taxes due for May and June of 2014. Mercury's attorney, in a conference call, explained to CCDOR that the tax was preempted by federal law and that they did not agree with CCDOR's position. CCDOR responded by issuing an "Amusement Tax Delinquency Notice of Jeopardy Tax Determination and Assessment" notice dated September 9, 2014, to Mercury advising that Mercury had not remitted taxes due for May through July of 2014. (Source: Appellate Court Opinion of Mercury Sightseeing Boats, Inc. v. County of Cook)

Mercury's attorney, before filing the Protest and Petition form, wanted to verify the protests' due date with CCDOR and this is what transpired:

Mercury ended up filing the protest and petition for hearing on October 1, 2014 and CCDOR forwarded it to the Cook County Department of Administrative Hearings (DOAH).

One of the arguments Mercury raised before the DOAH was that the amusement tax was preempted by 33 U.S.C. § 5(b) (2012) which is found under United States Code Title 33 NAVIGATION AND NAVIGABLE WATERS. (Source: Appellate Court Opinion of Mercury Sightseeing Boats, Inc. v. County of Cook)

The Administrative Law Judge on July 19, 2016 issued an opinion and decision and ruled that the amusement tax was preempted by 33 U.S.C. § 5(b) (2012). The ALJ, in this ruling also noted that the October 1st, 2014 filing of Mercury's protest was not timely filed under Cook County's Code of Ordinances but since CCDOR didn't raise this issue they forfeited this argument. (Source: Appellate Court Opinion of Mercury Sightseeing Boats, Inc. v. County of Cook)

After this decision, did CCDOR stop collecting amusement tax from all of the businesses operating Boat Rides/Tours? Of course not. Instead, CCDOR filed a complaint for administrative review in the circuit (trial) court arguing for the first time that Mercury's protest was untimely and thus DOAH lacked jurisdiction to hear the petition. CCDOR was brazen enough to claim this even after CCDOR's auditor had confirmed to Mercury that "the due date to file the protest is October 1, 2014".

The circuit court judge that reviewed the administrative hearing decision decided that Mercury had failed to meet the 20-day time limit to file a protest and determined that the deadline was jurisdictional and therefore the ALJ did not have the authority the hear the case, so they reversed and ordered that judgment be entered in CCDOR's favor. Mercury appealed the circuit court's decision to the Illinois Appellate Court and the judge decided that CCDOR "violated the procedural due process rights of Mercury by affirmatively misleading Mercury, if unintentionally, on the proper deadline for filing" So the appellate court vacated the trial court's ruling and remanded it to the the circuit court for a consideration of the final administrative decision on the merits. (Source: Appellate Court Opinion of Mercury Sightseeing Boats, Inc. v. County of Cook)

During this entire period from August 2014, when Mercury was first contacted to pay amusement tax on Boat Rides/Tours up until April of 2020, when CCDOR finally decided to notify businesses to stop collecting this tax, approximately 12 other businesses who also operated Boat Rides/Tours and who believed in what CCDOR was telling them, remitted approximately 5.5 million dollars in amusement taxes for a tax that was and still is preempted by federal law. This is CCDOR's version of fair and equitable treatment.

The Cook County Department of Revenue's mission is:

"To efficiently administer and equitably enforce compliance with Cook County Home Rule taxes while providing courteous and professional service to the public. To process Cook County fines, fees, and license applications in an accurate and timely Manner." (Source: CCDOR's homepage https://www.cookcountyil.gov/agency/department-revenue)

In this report, I provided a few examples of how CCDOR treated local businesses. It is clearly evident that CCDOR's treatment of these businesses was not courteous nor professional. CCDOR convinced businesses to collectively pay millions of dollars for unauthorized or preempted taxes. Those who ignored CCDOR's claims paid zero taxes. This is not fair and equitable enforcement. Furthermore, when CCDOR's positions failed in the courts, CCDOR made up any argument to keep these cases going in the court systems so they can keep collecting these taxes from the rest of the taxpayers.

When it came to Paid Television, CCDOR never had the authority to issue a ruling that expanded the scope of the definition of an amusement, but kept on insisting to businesses that they owed CCDOR money based on this ruling, even after the Board of Commissioners had rejected Paid Television as an amusement back in February 2011, and again in November 2015. For amusement taxes on both Paid Television and Boat Rides/Tours, CCDOR did not put a hold on collecting these taxes from other businesses when court cases regarding their validity were taking place. Instead, they continued to collect these unauthorized or preempted taxes from hundreds of businesses during these prolonged court cases, and well after judgements were entered against CCDOR. By using these tactics, CCDOR collected over 8.5 million dollars from businesses that believed in what their local government was telling them. If you think CCDOR has refunded any of these businesses their money back after losing these court cases, think again.

The Cook County Department of Revenue enforces compliance by employing Field Auditors whose main job is to audit businesses by reviewing their books and records to see if they are in compliance with the Cook County Home Rule Tax Ordinances. But from the examples I provided in this report and from my own personal experience, CCDOR's management demands their field auditors make sure businesses are compliant with CCDOR's position (management's interpretation of the Ordinance) which in many cases conflicts with the language of the Ordinances. In making their positions (interpretations), CCDOR disregards what is written in the Ordinances, and is mainly concerned with creating positions that will expand the current tax base with the goal of bringing in more tax revenues. CCDOR's managers do not think their positions are unlawful, because they believe they have the authority to interpret the Ordinances any way they please.

So how do I know all of this? I was employed by CCDOR between February of 2013 through May of 2023. For the first three years I was CCDOR's sole internal auditor, and from January 2016, I was a field auditor who audited businesses. As a field auditor, CCDOR's management demanded I use their positions (their interpretations of the Ordinances) when auditing businesses and assessing tax liabilities. They would also force me to defend these questionable "positions" when testifying as an auditor in Administrative Hearings proceedings. I tried to reason with management, but when I would disagree with their interpretations and refuse to go through with their demands, they would yell at me furiously, use profanities, and threaten to discipline me if I did not stick to their plan.

I notified the Cook County Office of the Independent Inspector General (OIIG) about CCDOR's management and their tactics on a few occasions. The first time was in November of 2018 regarding a Motor Fuel Tax audit that I had been assigned, and more recently in November of 2022 regarding management's unethical practices. I have provided the OIIG investigators details of CCDOR's questionable tactics, including the "Paid Television" amusement tax scheme, and other evidence of CCDOR's managers committing what I believe to be violations of Cook County's personnel rules, and violations of state & federal laws. As of today, nothing has been done to discipline CCDOR's managers. In fact, the opposite has happened. Since November 2018, every member of CCDOR's management team that was responsible for these schemes has been promoted to very high positions within Cook County Government.

My name is Ktisifon Tselentis, and I founded the Cook County Avenger to help businesses fight these unfair and unethical practices. If your business was affected by the schemes mentioned in this report or if you have been subjected to an unfair tax audit and/or tax assessment and would like for us to help, please send us an email at contact@ccavenger.com or leave us a message in the contact section of our webpage.